In 2 Reasons Rate Rise Makes Homebuilders A Buy, I described how rising interest rates will likely boost home sales, not weaken them. Two important forces could be unleashed by a rate uptrend. First, potential home buyers can be influenced to act sooner, thereby avoiding higher mortgage rates later. Second, banks, seeing an increase in interest (profit) margin coincident with a reduction in refinancing fees, can be driven to readopt their more normal mortgage loan activity by allocating more funds and relaxing their stringent borrower requirements.

Mortgage rates up = home demand increase? Isn't that illogical?

I know the proposition that rising rates will spur buyers can seem illogical. However, history has seen such results. The key is the environment in which the rate rise occurs. Today's is perfect.

First, the rental market's expansion means the pool of potential home buyers has grown even as household formations produce even more demand. No, the rental rise is not a cultural shift. Owning a home continues to be the American dream. Many renters, as has happened previously, want to buy. Lingering housing market concerns, expectations of continuing low mortgage rates and lenders' stringent requirements have helped buyers hesitate and enlarge this potential demand. The triple-combination of good news (see next), rates rising and (soon) lenders' switching gears to less stringent policies will push those delaying buyers to act.

Second, the word is out, often occurring on the front page of local newspapers: House prices are up and the inventory of houses for sale is down. Importantly, this heating up began prior to the summer selling season, highlighting the strength of the move.

Third, owners "stuck" in houses with little or no equity are seeing their situation improve significantly. The pent-up desire to move to another home (for whatever reason) will help both the existing sale market (boost quality inventory and maintain/improve average prices from non-desperate sales) and new home sales.

Fourth, homebuilders are active again, promoting shiny, new houses with the modern designs, desired sizes, eco-friendly characteristics, up-to-date fixtures/appliances and enticing optional features. That new paint smell in a sparkling new community remains highly desirable. Moreover, homebuilders provide financing support if not pre-arranged packages (and appraisals are not a problem).

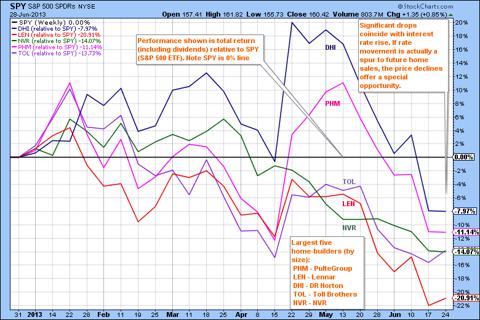

The stock market's simplistic reaction to interest rate increases has produced a significant opportunity

Driving down the homebuilder stocks recently is the simplistic view that higher rates necessarily hurt home sales. Here is how the leading homebuilder stocks have fared (relative to the stock market) as interest rates have turned up.

(Click to enlarge)

(Stock chart courtesy of StockCharts.com)

Note that last week saw a leveling off from the recent drop. I believe the cause is that the simplistic reasoning is giving way to a more fulsome analysis. Even the AP voiced the alternative analysis in 30-Year Mortgage Rate Highest in Two Years:

In the short run, the spike in mortgage rates might be causing more people to consider buying a home soon. Rates are still low by historical standards, and would-be buyers would want to lock them in before they rise further.

Obviously, if rising interest rates actually spur home sales, the significant stock drops have produced an excellent risk/return situation - a special return opportunity with sharply reduced risk. To take advantage, we then need to decide how to invest. There are three strategies.

Investment strategy #1 - Select homebuilder ETFs

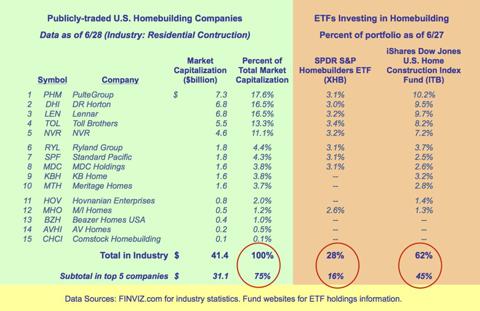

Since the residential construction industry is where we see the opportunity, a first thought is to invest in a homebuilder exchange-traded fund (ETF). Such a one-stop choice can provide both the focus and the diversification that many investors prefer. For homebuilding (residential construction), there are two choices:

SPDR S&P Homebuilders ETF (XHB): This ETF, with $2.6 billion in assets, mirrors the S&P Homebuilders Select Industry Index

iShares Dow Jones US Home Construction Index Fund (ITB): This ETF, with $2.3 billion in assets, mirrors the Dow Jones US Select Home Construction Index

There is a drawback in both of these funds, however. As the table shows, these two major ETFs investing in the "homebuilder" industry are diversified beyond the "pure" residential construction companies.

(Click to enlarge)

Each ETF has holdings (72% of XHB's assets and 38% of ITB's assets) that are in housing-related companies, such as Home Depot (HD) and Ethan Allen Interiors (ETH). While these broader portfolios offer risk reduction from industry diversification, they also dilute the opportunity we are pursuing from homebuilders, alone.

Investment strategy #2 - Create a homebuilder stock portfolio

To focus only on homebuilders, we must invest in individual stock(s). Looking at the listing and sizes in the table, above, two portfolio strategies look reasonable.

The first approach is to buy the top five builders. These companies, somewhat similar sized, account for 75% of total industry capitalization.

The second approach is to diversify further, perhaps adding the next five similar sized firms. The second five are much smaller, so it would be best not to equal weight the ten. For example, based roughly on the market capitalization differences between the two groups, a size-based portfolio could hold 16% in each of the top five (80% total) and 4% in each of the next five (20% total).

A problem: Homebuilder diversification has too much risk

While homebuilders look to have good growth potential, we need to invest carefully because homebuilding is a high-risk industry. It rides a dual sales cycle: Housing first, then, sitting atop that, new housing. Moreover, costs (land, labor, materials, selling and financing) have their own, coincident cycles. Add to that the need for advance commitments (location selection, land purchases, community/housing designs, site prep, construction equipment, skilled laborers, and marketing), all the while maintaining profitable, yet competitive, pricing.

While all those issues appear to argue for management conservatism, homebuilder success actually requires aggressiveness - both to take advantage of good markets and to avoid being seriously harmed in poor ones.

Investment strategy #3 - Select one homebuilder

It's those issues (the need for aggressiveness in a high risk, highly cyclical business) that argue for not diversifying. Rather, I believe the best investment approach is to focus on the one homebuilder (or two or three, if you must) with the best management team, measured in terms of skill, experience/longevity and proven success. My preference is to select from among the top five, because I believe each has access to the resources needed plus each operates in a broad range of markets (this location diversification is important). In addition, because the management aggressiveness needed for success is similar to entrepreneurial aggressiveness, I prefer two characteristics: Open communications (both good and bad) with shareholders, and results-based incentives.

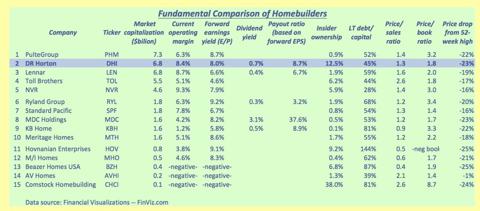

Starting with a fundamental comparison of the companies, D.R. Horton (DHI) came out on top. Below are the items I weight the most.

(Click to enlarge)

Besides having generally attractive fundamentals, D.R. Horton is especially noteworthy for the high insider ownership, the lower debt/capital ratio and the attractive forward earnings yield.

Not shown in the table above are some other fundamentals typically used to analyze "normal" stocks, but currently are irrelevant given where we are in the housing cycle (e.g., past growth rates in sales and earnings). So, to delve further, we need to rely on other analytical approaches. As described below, I found D.R. Horton to possess and exhibit all the strengths necessary for success with controlled risk, making it an ideal investment to ride the homebuilder cycle.

First, the executive team - It has the desired levels of skill and experience/longevity. Here are the three, key figures:

- Donald R. Horton - Chairman and D.R. Horton founder (company IPO was in 1992)

- Donald J. Tomnitz - Vice Chairman, CEO (since 1998) and President (since 2000)

- William W. Wheat - CFO and Executive Vice President (both since 2003)

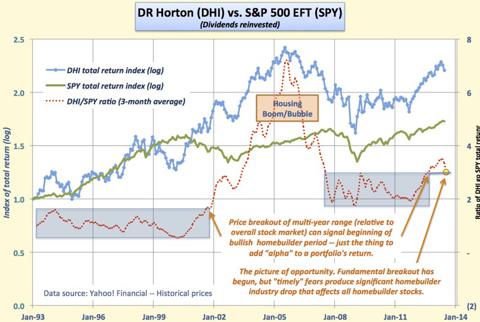

Second, DHI's performance - While necessarily affected by the homebuilder cycle, the stock has made long-term progress.

(Click to enlarge)

Importantly, as noted in the graph, the stock's relative performance rising to a new multi-year high is an important indicator of possible superior returns ahead.

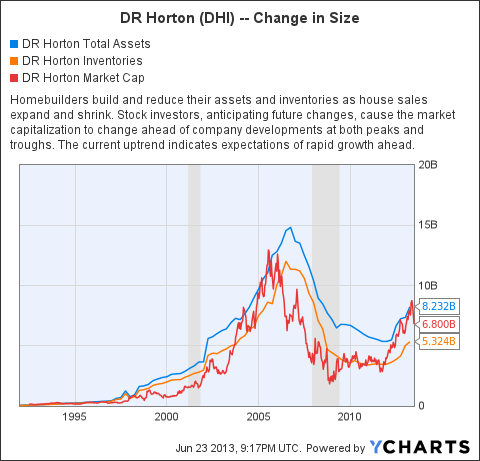

Third, the relationship between the balance sheet growth and the stock's growth - The comparison of assets & inventories (both company growth measures) to market capitalization (stock valuation/growth measure) shows both the long-term growth and the developing, positive current trends.

(Click to enlarge)

DHI Total Assets data by YCharts

As we would expect, future-focused investors drive market capitalization (i.e., stock price) moves ahead of fundamental shifts. Therefore, the fact that the latest market capitalization rise is faster than assets & inventories is a vote of confidence, not an indication of overvaluation.

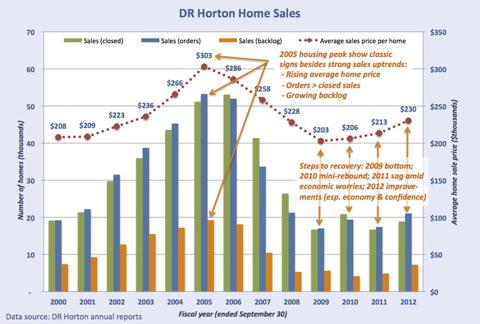

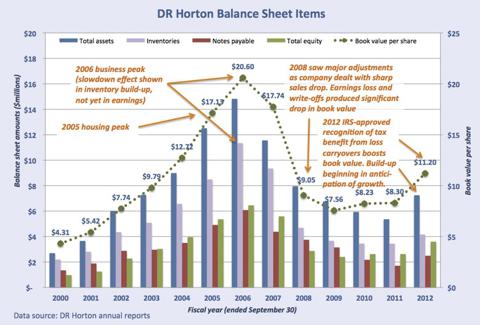

Fourth, the annual reports year-by-year provide two important insights: (1) How the company fared over the various cycle periods (up, down and current), and (2) how management explained the environment changes, the company's results and the best strategy to follow.

The data, shown in the two graphs below, reflect the company's results and strategies over the complete housing cycle.

(Click to enlarge)

(Click to enlarge)

Each annual report contains Chairman and founder Donald R. Horton's personal description of both what happened and reasons why. He then explains how the company reacted and what the goals and strategies are for the next year. Annual reports for the past nine years are available on the company's website. (The important information is presented in the front: First, one page of charts and tables showing the past five years of key data; then, Chairman Donald R. Horton's letter to shareholders.)

In each year's letter to shareholders, management's skill and experience come through as well as an important characteristic of a successful entrepreneur in a high risk, cyclical business: Realistic foresight. (At the end of this article, I've included two excerpts - the first from troubled 2008, and the second from improving 2012.)

The bottom line

It appears homebuilders are entering a new uptrend. Given the Great Recession's adverse affects, we can expect sizeable pent-up demand for new housing to emerge that could produce large gains in homebuilder stocks. Of the publicly traded homebuilders, D.R. Horton appears especially well-positioned to perform well.

A potential bonus: Scarcity can drive stocks up when investors turn bullish

Occasionally, we get forecasts of the stock market moving because of shifts in demand. More realistically, however, such relative performance moves are in subsets of stocks. The fewer the stocks and the smaller the companies, the more pronounced the effect can be. This potential is especially relevant in a cyclical industry like homebuilding, where investors run hot, then cold, and back again.

Here's why homebuilder stocks could get an extra push if they became desired by investors:

- As shown above, there are only 15 publicly traded companies, and size is skewed to the top five [three of which are in the S&P 500: PulteGroup (PHM), D.R. Horton and Lennar (LEN)].

- PulteGroup, with the largest market capitalization, ranks below more than 450 larger U.S. companies (excluding ETFs).

- Perhaps most relevant are the comparisons to the home improvement stores. The market capitalization of Lowe's (LOW) is $45 billion, more than the $41 total for all homebuilders. Home Depot's is $114 billion, almost three times the total.

In other words, an increase in investor interest could spark a nice run in the homebuilder stocks. (While not a reason to buy, it's nice to know that, if fundamental growth comes through, there is a stock price accelerant in the wings.)

--------------------

Addendum: Excerpts from D.R. Horton 2008 and 2012 annual reports

For the fiscal year ended September 2008, Horton's comments are especially important. With homebuilding having peaked three years earlier and the financial crisis + Great Recession now is full swing, homebuilders were suffering significantly. How they viewed the situation and the actions they took would determine the eventual strength and potential of the firms.

From Donald R. Horton's 2008 letter to shareholders:

Our fiscal 2008 results reflect the challenges that the homebuilding industry faced during the year. During fiscal 2008 the factors hurting demand for new homes became more intense and pervasive across the United States. As a result, the already difficult conditions within the industry became progressively more challenging.

High inventory levels of both new and existing homes, elevated cancellation rates, low sales absorption rates and overall weak consumer confidence persisted throughout the year. The effects of these factors were further magnified by credit tightening in the mortgage markets, increasing home foreclosures and severe shortages of liquidity in the financial markets. The liquidity shortage has caused concern about the viability of many financial institutions and has negatively impacted the already weakening economy, which has created fears of a prolonged recession. These factors, combined with our continued elevated sales cancellation rate, caused our sales volume to be significantly reduced. Also, our gross profit from home sales revenues continued to decline as we offered higher levels of incentives and price concessions in attempts to stimulate demand in our communities.

As we progressed though fiscal 2008, our disappointing sales results, further declines in our sales order prices, continued declines in our gross profit from home sales revenues and the more challenging market conditions caused our outlook for the homebuilding industry to remain cautious. We believe that housing market conditions may continue to deteriorate, and that the timing of a recovery in the housing market remains unclear. Our outlook incorporates several factors, including continued margin pressure from sales price reductions and incentives; continued high levels of new and existing homes available for sale; weak demand from new home consumers; continued high sales cancellations; significant restrictions on the availability of certain mortgage products and an overall increase in the underwriting requirements for home financing as a result of the recent credit tightening in the mortgage markets.

During fiscal 2008, particularly in the fourth quarter, we sold a significant amount of land and lots through numerous transactions to generate cash flows, reduce our future carrying costs and land development obligations, and lower our inventory supply in certain markets to match our expectations of future demand.

Consummating these transactions during the current fiscal year allowed us to monetize a larger portion of our deferred tax assets through a loss carryback to fiscal 2006 resulting in an increase in our expected tax refund.

Due to the declining market conditions discussed above, we evaluated a significant portion of our inventory in our quarterly impairment analyses during fiscal 2008. Additionally, we evaluated the recoverability of our goodwill. Our goodwill and inventory impairment evaluations reflected our expectation of continued and increasing challenges in the homebuilding industry, and our belief that these challenging conditions will persist for some time. Based on our evaluations and as a result of our fourth quarter land and lot sales, we recorded significant impairment charges to our inventory and goodwill balances during the year, which materially affected our operating results during fiscal 2008.

------------------------

Now we can shift to September 2012 so see how management is focusing on a more positive outlook. Doing so gives us an understanding of what we can expect should things work out. Also, it gives us a good reading of management's objectivity as things turn up - i.e., are they overly focused on the growth potential, or do they have a more balanced outlook. Donald R. Horton's 2012 annual report view, like those in previous years, remains balanced.

From Donald R. Horton's 2012 letter to shareholders:

In fiscal 2012, D.R. Horton, Inc. capitalized on the emerging improvement in the U.S. housing market and strengthened its leading position in the homebuilding industry. For the 11thconsecutive fiscal year, we closed more homes than any other homebuilder in the United States, and we generated our highest profit in six years. We gained market share, increased our investments in inventory and raised capital to prepare for future growth. With our broad geographic base and financial strength, we are poised to increase our market share further while retaining the operational flexibility to respond to uncertain economic conditions. Our financial achievements during fiscal 2012 included the following:

29% increase in the value of net sales orders;

20% increase in total revenues;

$243 million of consolidated pre-tax income, up $231 million from a year ago;

$3.6 billion of total equity, up $1.0 billion from a year ago; and

$1.7 billion sales order backlog, up 61% from a year ago

Our 2012 financial performance is the result of the tremendous efforts of our homebuilding and financial services teams who worked tirelessly throughout the six-year housing recession to rebuild a profitable business in an extremely challenging market. To achieve profitability at a relatively low closings volume, we focused on the fundamentals of selling homes, providing high quality customer service, adjusting our product offerings based on customer demand, managing our investments in inventory, reducing SG&A and financing costs and improving gross margins through controlling construction costs. We also prepared for the eventual improvement in demand by selectively investing in our business through opening new communities and entering new markets. Although the U.S. economy remains weak and the mortgage-lending environment is restrictive, we believe that our revenues and pre-tax income will increase again in fiscal 2013.

Our strong balance sheet and liquidity are supporting our financial performance and growth potential. We raised capital in 2012 by issuing $700 million of senior notes at company-record low interest rates, and we recently obtained $600 million in bank lending commitments through a new revolving credit facility. Our $1.3 billion of homebuilding cash and marketable securities and our 39.1% ratio of gross homebuilding debt to total capital (21.4% net of cash and marketable securities) provide significant flexibility for us to invest in our business and take advantage of profitable growth opportunities. Our number of homes in inventory and our lot supply increased 24% and 35%, respectively, from a year ago, reflecting investments in our existing markets and entry into new markets.

The outlook is uncertain for the U.S. economy, the job market and potential changes in government policies that will affect the housing market, and we believe that significant and sustainable long-term growth in the U.S. housing market will require an improvement in economic conditions. We will continue to compete for market share in this environment by building high quality homes that offer compelling value to homebuyers, assisting each of our customers during their home purchase and financing process and providing reliable service to our new homeowners. We will also operate our business in a capital efficient manner by remaining disciplined in our investments in land, managing our inventory of owned lots and homes in line with sales demand, and controlling our construction, SG&A and interest costs. Finally, we will adjust our operating strategies as needed to remain competitive and profitable with a strong balance sheet and liquidity position.

Disclosure: I am long DHI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: http://seekingalpha.com/article/1528892-d-r-horton-built-to-ride-housing-s-new-upswing

Electoral College chuck pagano A Gay Lesbian daylight savings time 2012 Where To Vote james harden breeders cup

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.